Streamlined Energy and Carbon Reporting (SECR)

We help organisations comply with Streamlined Energy and Carbon Reporting by auditing and reporting on the energy consumption and carbon emissions.

Streamlined Energy and Carbon Reporting (SECR) is a legal requirement for all large organisations to disclose their energy and carbon emissions within their Annual Director’s Report, or separate sustainability report. Large companies and Limited Liability

Partnerships (LLPs) under SECR are defined as meeting at least two of the following three criteria:

- Turnover exceeding £36m;

- Balance sheet exceeding £18m;

- 250 or more employees

Furthermore, quoted companies of any size, listed on a major stock exchange, and incorporated in the United Kingdom must also report.

SMEs are encouraged to participate in SECR, as it represents best practice in environmental disclosures and helps to identify opportunities to reduce environmental impact and save money.

Benefits

- Our experts can assist any organisation to audit their organisation and prepare their report.

- Our reports present total energy and GHG emissions as well as metrics so performance can be compared year on year.

- Support with drafting ‘environmental narrative’ stating what the company has done to reduce energy and carbon consumption.

- Reporting includes a comparison with the previous results, as well as on-going long-term analysis.

- Emissions are reported in tonnes of carbon dioxide equivalent (CO2e), including all seven major greenhouse gases.

Experience

Understanding

Rationalising data

Efficiency

Accurate

Process

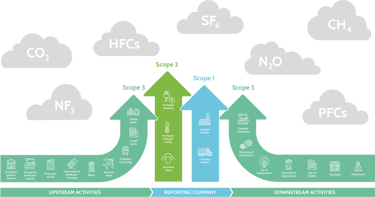

Organisations are required to report on the energy consumption and carbon emissions associated with their Scope 1 and 2 emissions as well as employee mileage from Scope 3.

They should present the total for each as well as the metrics so performance can be compared year on year.

The report should include an ‘environmental narrative’ which states what the company has done during the last 12 months to reduce energy and carbon consumption. There is no standard for this and companies should make the statement bespoke to them. There is, however, a template in the guidance which provide a basis format to work to.

A comparison with the previous reporting year is required, and on-going long-term analysis is encouraged.

Emissions must be reported in tonnes of carbon dioxide equivalent (CO2e), which includes all seven major greenhouse gases.

Our experts can assist any organisation to audit their organisation and prepare their report.

SECR is required for Unquoted Large Companies and LLPs and Quoted Companies.

Unquoted Large Companies and LLPs are required to report the following:

- UK energy consumption.

- UK Scope 1 emissions (directly combustible fuels).

- UK Scope 2 emissions (purchased electricity, heat and steam) emissions.

- UK Scope 3 emissions (rental vehicles, business mileage claims).

Scope 3 emissions only cover business travel where the company is supplied with fuel but not where fuel is paid for indirectly. For example, fuel is consumed in personal vehicles and hire cars (and reimbursed by the company either exactly or at a set rate) but fuel associated business flights, trains or taxis are excluded, as the vehicles are not operated by the company or its employees.

However, companies are strongly encouraged to report other sources of Scope 3 emissions relevant to their business. These may include other forms of business travel, materials, waste, employee commuting, homeworking, transport of goods etc.

Whilst not mandatory, external verification or assurance is recommended to ensure accuracy, completeness of reporting.

Quoted Companies are required to report the following:

- Global energy consumption.

- Global Scope 1 emissions (directly combustible fuels, natural gas, petrol, diesel, oil etc.).

- Global Scope 2 emissions (purchased electricity, heat and steam).

- Emissions for UK and overseas must be reported separately.

- At least one key performance indicator to show the link between carbon emissions and business performance.

Scope 3 emissions are voluntary for quoted companies. However, it is becomingly increasingly expected that companies account for and tackle emissions with their supply chains.

You might also be interested in...

Your environmental risk reduction partner, ensuring the safety of your people, property, reputation and the environment

Our experts are on hand to provide tailored investigation, consultancy, response and remediation services to help you balance commercial objectives and environmental compliance.

Contact our experts